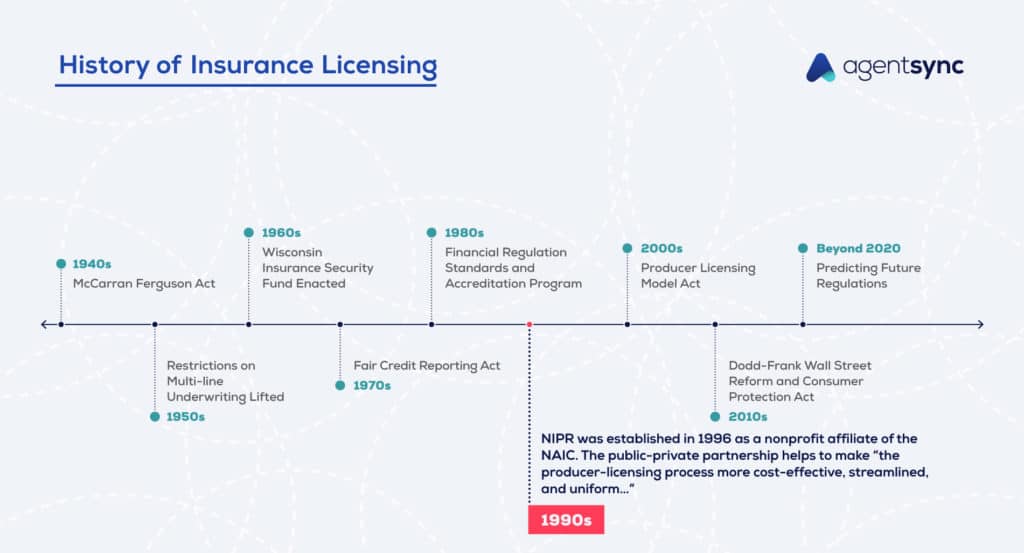

Introduction

The insurance industry has a long history that has evolved over centuries. Understanding its historical perspective can provide insights into its importance in society today.

Brief overview of the insurance industry and its importance in society

Insurance is a system that transfers the risk of potential financial loss from an individual or business to an insurance company. It provides protection and financial security in case of unforeseen events such as accidents, illnesses, or natural disasters. The concept of insurance dates back to ancient civilizations, where merchants would pool their resources to spread the risk of lost goods during long and dangerous journeys. Over time, the insurance industry has grown and adapted to meet the changing needs of individuals and businesses. Today, it plays a crucial role in providing peace of mind, stability, and protection for individuals, families, and businesses around the world. From life insurance to property insurance, health insurance to car insurance, the industry has expanded to cover various aspects of our lives. As society continues to evolve, the insurance industry continues to innovate and adapt to new risks and challenges. Its historical development showcases how it has become an integral part of our modern society.

Origins of Insurance

Historical background of insurance and its early forms

The insurance industry has a long and fascinating history. It dates back to ancient times when merchants and traders sought ways to mitigate the risks associated with their businesses. In these early days, insurance took various forms, such as collective agreements among groups of merchants to share losses due to theft or shipwrecks. In fact, the concept of “bottomry” emerged in ancient Babylon, where loans were made to merchants with the understanding that repayment would be waived if their goods were lost at sea.

Over time, insurance evolved and became more structured. The modern insurance industry as we know it today can trace its roots back to the establishment of Lloyd’s of London in the late 17th century. Lloyd’s started as a coffee house where people would gather to discuss maritime affairs and negotiate insurance contracts.

Throughout history, various types of insurance emerged to meet different needs. For example, life insurance became popular in the 18th century to provide financial security for families in case of the breadwinner’s untimely death. Fire insurance also gained prominence during this period, as urbanization led to increased risks of property damage from fires.

The growth and evolution of the insurance industry continued through the industrial revolution and into the modern era. Today, insurance plays a vital role in protecting individuals, businesses, and society as a whole against a wide range of risks.

Overall, understanding the historical background of the insurance industry helps us appreciate how it has developed and adapted over time to meet the changing needs of individuals and businesses alike.

The Evolution of the Insurance Industry: A Historical Perspective

Early Insurance Practices

Insurance, in various forms, has been around for centuries. In ancient civilizations and early societies, there were already practices in place to protect against risk. In Babylonia, merchants would pay lenders an extra amount in case their shipments got lost or damaged. The Greeks and Romans had similar systems to safeguard against sea voyages gone wrong. These early insurance practices paved the way for the modern insurance industry we know today. With time, insurance has evolved to cover a wide range of risks, from property and health insurance to life and business insurance. The concept of pooling resources to share the burden of potential losses remains at the core of insurance. As society continues to face new risks and challenges, the insurance industry continues to adapt and provide solutions to protect individuals and businesses alike

Evolution of Insurance in Modern Times

The growth and transformation of the insurance industry during the 18th and 19th centuries

The insurance industry has come a long way since its inception. In the 18th and 19th centuries, it experienced significant growth and transformation.

During this period, insurance companies emerged to provide coverage for various risks, such as fire, marine, life, and health insurance. The need for such coverage became more apparent as industrialization and globalization expanded.

In the 18th century, Lloyd’s of London gained prominence as an insurance market, specializing in marine insurance. The establishment of mutual insurance societies and friendly societies also played a crucial role in providing affordable coverage to individuals and communities.

The 19th century witnessed the development of actuarial science, which allowed insurance companies to assess risks accurately and calculate premiums accordingly. This led to the expansion of life insurance and the emergence of new types of coverage, such as accident and liability insurance.

Overall, the growth and transformation of the insurance industry during the 18th and 19th centuries laid the foundation for its continued evolution in modern times. Insurance companies continue to adapt to changing risks and market demands, offering a wide range of coverage options to individuals and businesses alike.

Rise of Insurance Companies

The establishment and expansion of insurance companies in the 20th century

The insurance industry has come a long way since its inception. In the early 20th century, insurance companies began to emerge and expand rapidly. As people recognized the need for protection against unforeseen events, these companies played a vital role in providing coverage for individuals and businesses.

During this period, insurance companies started offering a wide range of policies to meet various needs. Life insurance policies became popular, providing financial security for families in case of unexpected death. Property and casualty insurance also gained traction, helping businesses and individuals safeguard their assets from potential risks such as fire, theft, or accidents.

The expansion of insurance companies was fueled by several factors. Advances in technology enabled better risk assessment and underwriting processes. The establishment of regulatory bodies ensured consumer protection and stability within the industry. Additionally, increased public awareness about the importance of insurance and growing economic prosperity led to a higher demand for coverage.

Over time, insurance companies adapted to changing market dynamics and expanded their offerings to include health insurance, automobile insurance, and more specialized policies. They embraced digital advancements to streamline operations and provide better customer service.

Today, the insurance industry continues to evolve, leveraging data analytics, artificial intelligence, and blockchain technology to enhance risk management and improve efficiency. With a rich historical foundation, insurance companies have become an integral part of modern society’s risk management landscape.

In conclusion, the establishment and expansion of insurance companies in the 20th century revolutionized how individuals and businesses protect themselves against various risks. Their evolution continues to shape the industry’s landscape, ensuring that insurance remains a vital tool in mitigating unforeseen events.

Word Count: 258 words

Technological Advancements and Insurance

The impact of technology on the insurance industry and its evolution in the digital age

In the modern world, technology has revolutionized many industries, and the insurance industry is no exception. Advancements in technology have had a significant impact on how insurance companies operate and offer their services. From online policy purchasing and claims management to advanced data analytics and personalized pricing, technology has transformed the insurance landscape.

Gone are the days of lengthy paper applications and manual underwriting processes. Today, customers can easily purchase insurance policies online, compare quotes from multiple providers, and manage their policies through user-friendly web portals or mobile apps.

Furthermore, technologies like artificial intelligence (AI) and machine learning are being used to streamline claims processing and fraud detection. Claims can now be submitted digitally, and intelligent algorithms can analyze data to detect patterns indicative of fraudulent activities.

The digital age has also enabled insurance companies to gather vast amounts of data on policyholders, allowing them to offer personalized coverage options and pricing. With the help of data analytics, insurers can assess risks more accurately, leading to fairer premiums for customers.

Overall, as technology continues to advance, the insurance industry will continue to evolve. Insurers must adapt to these technological changes to stay competitive and meet the evolving needs of their customers.

Technological Advancements and Insurance

The impact of technology on the insurance industry and its evolution in the digital age

In the modern world, technology has revolutionized many industries, and the insurance industry is no exception. Advancements in technology have had a significant impact on how insurance companies operate and offer their services. From online policy purchasing and claims management to advanced data analytics and personalized pricing, technology has transformed the insurance landscape.

Gone are the days of lengthy paper applications and manual underwriting processes. Today, customers can easily purchase insurance policies online, compare quotes from multiple providers, and manage their policies through user-friendly web portals or mobile apps.

Furthermore, technologies like artificial intelligence (AI) and machine learning are being used to streamline claims processing and fraud detection. Claims can now be submitted digitally, and intelligent algorithms can analyze data to detect patterns indicative of fraudulent activities.

The digital age has also enabled insurance companies to gather vast amounts of data on policyholders, allowing them to offer personalized coverage options and pricing. With the help of data analytics, insurers can assess risks more accurately, leading to fairer premiums for customers.

Overall, as technology continues to advance, the insurance industry will continue to evolve. Insurers must adapt to these technological changes to stay competitive and meet the evolving needs of their customers.

Title

Title

Text

Current Trends and Future Outlook

Key trends shaping the insurance industry today and predictions for the future

With constant advancements in technology and changing consumer needs, the insurance industry is going through a significant transformation. Here are some key trends shaping the industry today and predictions for the future.

- Digitalization: The rise of digital tools and platforms has revolutionized the insurance industry, providing customers with convenient access to policies, claims, and information. In the future, expect to see increased use of artificial intelligence, machine learning, and automation to simplify processes and enhance customer experience.

- Personalization: Customers now expect personalized insurance products tailored to their unique needs. Insurance companies are leveraging data analytics to understand customer preferences and offer customized solutions. This trend will continue to grow as insurers embrace advanced analytics and predictive modeling.

- On-demand Insurance: The rise of sharing economy platforms has led to the emergence of on-demand insurance. People are looking for flexible coverage that can be activated or deactivated based on their specific needs. This trend is likely to expand further as new business models continue to disrupt traditional insurance practices.

- Cybersecurity: With increased reliance on technology, cybersecurity has become a top concern for insurance companies. Protecting sensitive customer data from cyber threats will remain a major focus in the future, with insurers investing in robust security measures and developing innovative solutions to mitigate risks.

- Sustainability: The growing importance of sustainability will impact the insurance industry as well. Insurers will be under pressure to develop environmentally friendly products and support sustainable initiatives.

Overall, the insurance industry is adapting to a rapidly changing landscape driven by technology, customer expectations, and global challenges. Keeping up with these trends will be crucial for insurers to remain competitive in the future market.

Conclusion

Summary of the insurance industry’s historical evolution and its significance today.

The insurance industry has experienced significant evolution throughout history, adapting to changing circumstances and societal needs. From the early forms of insurance in ancient civilizations to the establishment of modern insurance companies, the industry has played a crucial role in managing risk and providing financial protection.

Insurance has expanded beyond traditional areas like life and property coverage to encompass various sectors, including health, automobile, and liability. Technological advancements have revolutionized the industry, enabling streamlined processes, faster claims settlements, and personalized customer experiences.

Today, insurance plays a vital role in safeguarding individuals, businesses, and economies. It provides peace of mind by mitigating financial risks associated with unforeseen circumstances. Insurance companies offer tailored solutions to meet individual needs, ensuring comprehensive coverage and prompt assistance when needed.

Furthermore, the insurance industry contributes to economic growth as it facilitates business expansion and investment by minimizing risks. It also encourages individuals to pursue innovative ventures, knowing that they are protected against potential losses.

In conclusion, the historical evolution of the insurance industry highlights its importance in society today. The industry continues to evolve as new risks emerge and customer expectations change. By addressing evolving challenges and embracing technological advancements, insurers can enhance their service offerings and provide greater value to their policyholders.