Are you a business owner in need of funding? The options can be overwhelming, but two common choices are invoice factoring and traditional bank loans. While both can provide the much-needed capital, they differ in various aspects. Invoice factoring involves selling your unpaid invoices to a third party for a discounted rate, while bank loans offer capital based on your credit and business operations. In this blog post, we’ll dive into the differences between these two financing options to help you decide which is right for your business.

I. Introduction

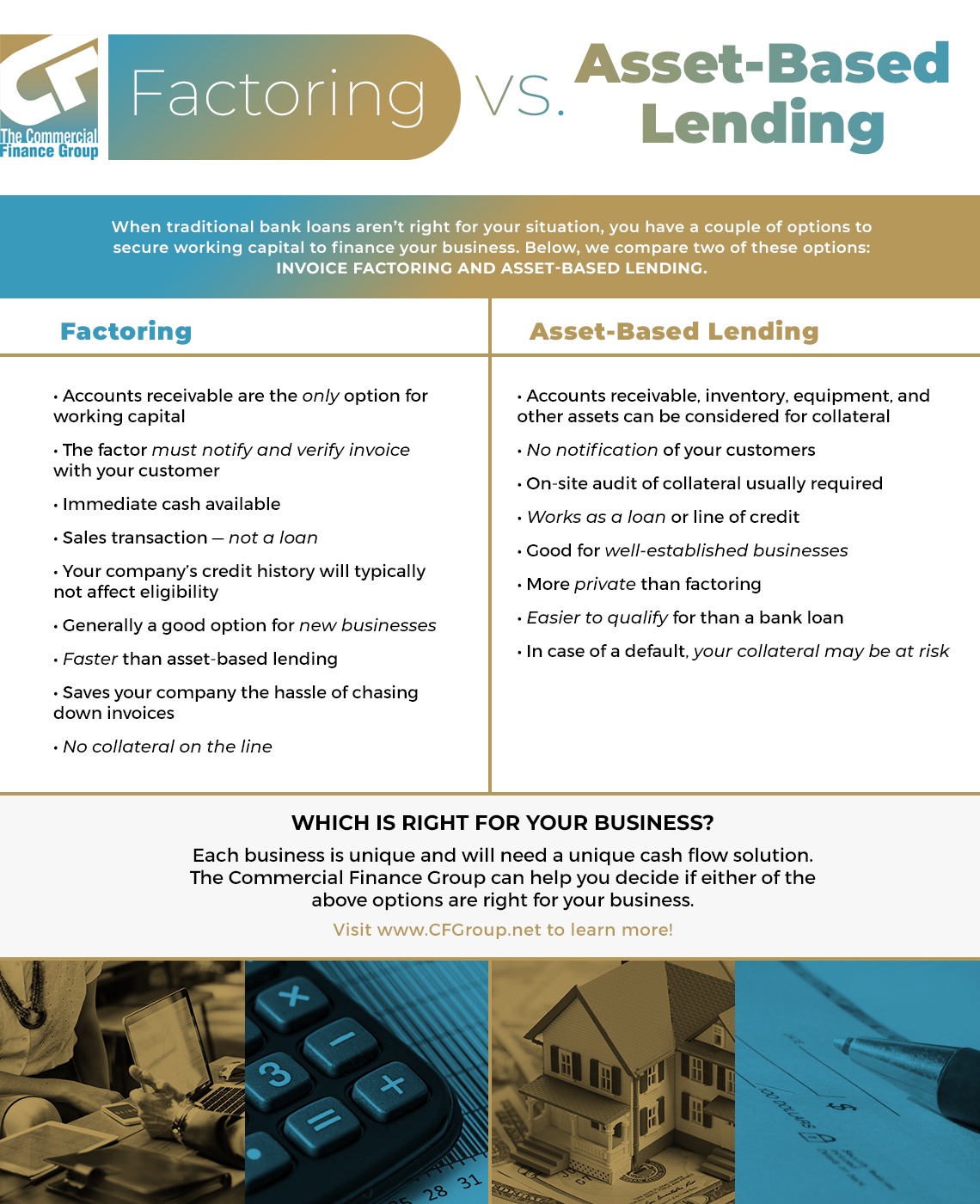

Explanation of the concept of invoice factoring and traditional bank financing

One of the primary ways businesses can receive funding is through traditional bank financing. However, the process can be lengthy and requirements strict, making it difficult for small businesses to secure loans. An alternative financing option is invoice factoring, where businesses sell their unpaid customer invoices to a factoring company for quick access to funds. The factoring company collects the payment from the customer and subtracts a fee before paying the remaining invoice amount to the business. Invoice factoring provides faster approval and more flexible financing options, making it a great choice for businesses with poor credit or limited operating history. [1][2]

Why businesses need funding

Every business, regardless of size or industry, needs funding at some point. Whether it’s to cover operating expenses, expand operations, invest in marketing, or meet payroll, having access to capital is crucial for business growth and success. However, traditional bank loans and lines of credit can be difficult to obtain, especially for small or early-stage businesses with limited credit history or collateral. That’s why alternative financing options like invoice factoring have gained popularity, providing a faster and more flexible source of cash flow for businesses in need. [3][4]

II. Invoice Factoring

Definition of invoice factoring

Invoice factoring is an alternative financing solution that helps businesses stabilize cash flow by unlocking the cash sitting in unpaid invoices. Rather than taking out a loan, you’ll be selling your invoices to a factoring company for immediate cash. As long as you have invoices to factor, funding is available. The amount of capital available grows with your business, and you get to choose which invoices you factor and how often. It’s a simple and debt-free business financing option that can yield unlimited growth for businesses of all sizes and stages. [5][6]

How it works

Invoice factoring is a straightforward concept that provides businesses with fast access to funds. In this process, business owners sell unpaid customer invoices to a factoring company for quick cash. The business owner receives cash for the invoice amount but less a factoring fee ahead of the payment terms. The customer responsible for paying the invoice instead pays the invoice amount to the factoring company according to the original payment terms. By leveraging the collection of a future customer payment, invoice factoring provides a predictable source of cash and flexible financing without creating debt. [7][8]

Advantages

One of the main advantages of invoice factoring over traditional bank financing is a faster approval process. With bank loans, it can take several months to receive a decision, and there’s no guarantee that you’ll even be approved for the loan. Invoice factoring, on the other hand, typically involves a streamlined online application process, and approval can be granted in as little as 24 hours. This speed and convenience can be crucial for businesses that need quick access to cash flow to cover expenses or take advantage of new opportunities. [9][10]

A. Faster approval process

One of the biggest advantages of invoice factoring over traditional bank financing is the faster approval process. With invoice factoring, the application process is usually quick and easy, often giving approvals within one business day. The factoring company reviews outstanding invoices and the creditworthiness of the companies that owe the business money to determine the advance rate, factoring cost, and additional fees. Once approved, businesses can typically receive immediate cash flow by having the factoring company deposit the funds into their bank account via ACH, wire, or fuel card. This quick access to funds can be beneficial for businesses with urgent financial needs. [11][12]

B. More flexible financing and funding limits

One of the advantages of invoice factoring over traditional bank financing is the flexibility it offers in terms of financing and funding limits. With factoring, the amount of available funding grows as the business’ receivables grow. This means that as your business grows, you will have greater borrowing flexibility available to you. In contrast, bank loans often come with a predetermined dollar limit, which can be difficult to increase once it has been reached. Invoice factoring offers a more scalable funding option that can adapt to your business’ needs. [13][14]

C. Approval based on customers’ creditworthiness and reliability

When it comes to invoice factoring, approval is largely based on your customers’ creditworthiness and reliability. This means that even if your own personal or business credit is not up to par, you may still be approved for financing. The factoring company evaluates the creditworthiness of your customers and uses that as a basis for approval. This makes invoice factoring an appealing option for individuals without a strong credit history or for businesses with customers who have a solid history of paying their invoices on time. [15][16]

D. Approval with poor credit

Having poor credit can make it difficult to secure traditional funding options such as bank loans. However, invoice factoring may be a viable alternative for businesses with less-than-perfect credit. Approval for invoice factoring is largely based on the creditworthiness and reliability of a business’s customers, not the business itself. This makes it a more appealing option for individuals without a strong credit history. With invoice factoring, businesses can access much-needed cash flow without the strict credit standards required by banks. [17][18]

E. Availability for working capital grows with business

One of the key advantages of invoice factoring is the flexibility it provides for growing businesses. As the company gains more customers and generates more invoices, the availability for working capital increases. Unlike traditional bank financing, where the amount of funding is predetermined and may not meet the needs of a growing business, invoice factoring can keep up with the demand for cash flow. This means that as a business expands and requires additional funding, it can continue to use invoice factoring to access the working capital it needs. [19][20]